首页

首页

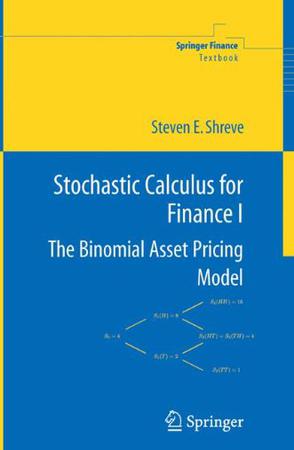

Stochastic Calculus for Finance Itxt,chm,pdf,epub,mobi下载

Stochastic Calculus for Finance Itxt,chm,pdf,epub,mobi下载作者: Steven Shreve 出版社: Springer 副标题: The Binomial Asset Pricing Model 出版年: 2004-4-21 页数: 187 定价: USD 54.95 装帧: Hardcover 丛书: springer finance ISBN: 9780387401003 内容简介 · · · · · ·Developed for the professional Master's program in Computational Finance at Carnegie Mellon, the leading financial engineering program in the U.S. Has been tested in the classroom and revised over a period of several years Exercises conclude every chapter; some of these extend the theory while others are drawn from practical problems in quantitative finance 作者简介 · · · · · ·卡耐基·梅隆大学的计算金融MSCF项目是美国金融工程的带头者,历史悠久,在华尔街亦享有盛誉。本书作者史蒂文·E施里夫(Steven E.Shreve)教授正是本号业的创办人之一,他经常和华尔街大公司的负责人们沟通,了解行业内新的发展趋势以在课程中加以改进,极大地促进了课程的优化。因而,由他所写的《金融随机分析》(第一、二卷)一直是随机分析在数罱金融领域应用方面的著名教材,许多世界名校将其作为金融工程专业的必修教材。 |

下载地址

引发思考

比较有兴趣

原以为会很枯燥

收到期待观看